The Complexity of Corporate Taxes

By, Davoud Ghasimi

In the US, President Donald Trump is pushing his plan for cutting taxes. The plan includes a big tax cut for corporations that reduces the federal tax rate for from the current level of 35% to possibly 20%. Trump’s administration argues that the tax reform will put more money in the hands of ordinary people and will generate more jobs and output. Of course, this is probably the usual way to publicly advertise and sell almost any plan. On the other hand, the opponents argue that this tax reform is likely to benefit investors only with close-to-zero long term impact on jobs and output, and as they argue, the US will end up with a bigger national debt. A good question probably is: does the US need a tax cut?

First, some definitions

According to the Tax Foundation, there are three measures of tax rate for corporations:

1- The statutory tax rate:

This is the tax on the next dollar of “taxable income”. This measure ignores any credit or deductions that reduce the liabilities. Companies look at this measure to decide about the location of profits.

2- The average effective tax rate:

This measure incorporates both the statutory tax rate and also any deduction or credit. This is basically the tax that companies pay divided by the pre-tax income, usually over a few periods to smooth out the short-term fluctuations. Companies use this measure to determine the location of their investments.

3- The marginal effective tax rate:

This is the tax on a marginal investment. The marginal tax rate determines incentives for making new investment in a given country.

A global comparison of corporate tax rates

Now let us take a look at the level of corporate tax rates around the globe. Here I present the summary of two different studies.

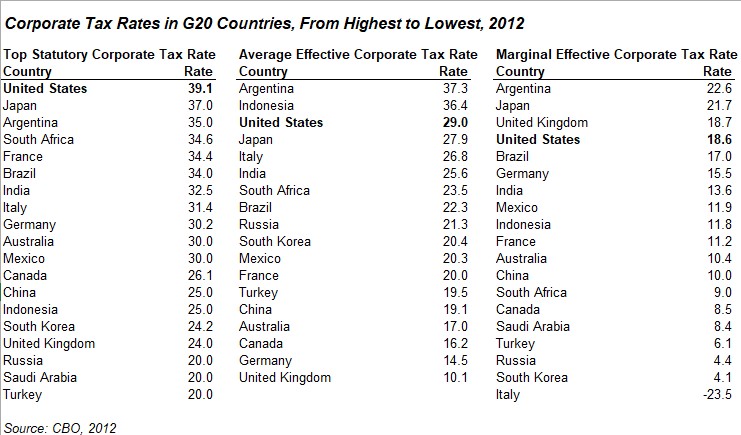

The first study from the CBO:

The table below is taken from a report published in 2012 by the US Congressional Budget Office (CBO). Formed in 1974, the CBO has worked as a non-partisan agency to produce “independent analyses of budgetary and economic issues to support the Congressional budget process”. As the table shows, the US ranks high on three measures of corporate taxes.

The second study from the ITEP:

While on the paper companies appear to pay higher taxes in the US, this study from the Institute on Taxation and Economic Policy (ITEP) suggests that “many corporations pay far less, or nothing at all, because of the many tax loopholes and special breaks they enjoy”. The ITEP is also a nonpartisan think tank but with reportedly more liberal views.

The ITEP published its findings in March 2017, in a report called “The 35 Percent Corporate Tax Myth”. They focused on 258 corporations from Fortune 500 for which they had detailed information, including federal and state taxes separately. According to the results, these companies paid only 21.2% in federal taxes from 2008 to 2015. This is well below the 35% statutory corporate tax rate and still smaller than 29% average effective corporate tax rate reported by the CBO.

There other findings as well. For example, “eighteen of the corporations, including General Electric, International Paper, Priceline.com and PG&E, paid no federal income tax at all over the eight-year period.” Also, “a fifth of the corporations (48) paid an effective tax rate of less than 10 percent over that period”.

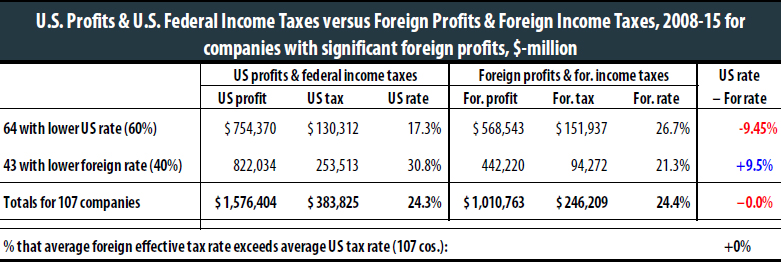

One important result probably is that the companies in the study paid a little higher taxes to foreigners compared to the taxes they paid in for their US business. The following table represents this result.

Table from “The 35 Percent Corporate Tax Myth” by the ITEP.

A third view?

While tax experts and economists or followers of different political camps can argue over the benefits and costs of the proposed tax reform, there is another person in the room who can possibly give you a less-biased answer: the market. As you know, the timing of the proposed tax cut is coincided with new records set by the US equity indices. In other words, investors are betting on higher returns in the future. How? According to the Reuters, CEOs of some biggest companies said in recent post-earnings calls that “they would use a tax reform windfall to buy back shares, retire debt and other shareholder-friendly moves”. And there are economic reasons for that as well. With an economy already close to the full-employment level, there is little incentive for companies to build new capacities and hire more workers.