Trader in Residence has concluded for the semester.

Written By Steven Klos

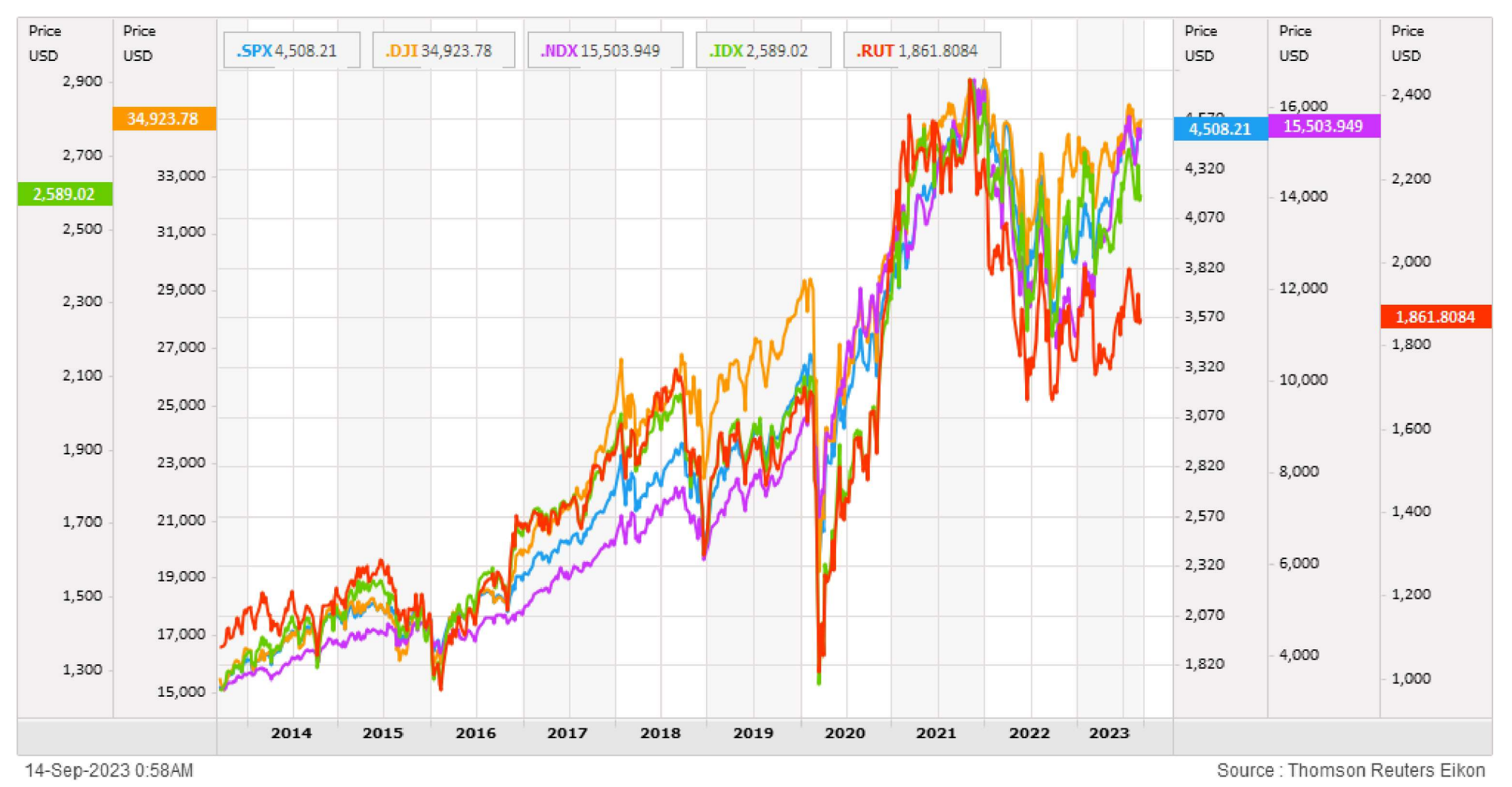

Investors were trying to downplay concerns about higher-than-expected inflation in the markets. This was because recent data indicated that inflation was staying relatively stable, which strengthened the belief that the Federal Reserve would likely keep interest rates unchanged, ...

Written by Yiming Wang

The Rise of the Electric Vehicle Industry

Nowadays, the rapid growth of the electric vehicle industry has become an inevitable trend all over the world. In 2017, the sales volume of Plug-in Electric Vehicle is only 17,763 in the U.S. However, the number has been through a more than 18 times growth to 326,644 in 2019. In 2020, one single company, Tesla, will achieve 500,000 electric vehicle deliveries by the end of the year. With the progress of battery technology and the breakthrough in autopilot development, the electric car is more and more efficient and convenient than before. In this trend, several new companies are standing out, who deliveries superior products and redefine the value of the electric vehicle.

Although the market share that electric vehicle has taken is still limited, the potential growth is huge. The transition from reliance on internal combustion engines to battery electric vehicles is essential for cutting greenhouse gas emissions and avoid the irreversible impacts of climate change. Achieving net-zero greenhouse gas emissions by 2050 has become the consensus between different governments. In the U.S, the 100% EV sales policy for 2035 or earlier has been throughout the Democratic primaries and got Joe Biden’s favour. In the EU, it is planned that the production of electric vehicles will exceed 4 million by the carmakers. In China, the government has planned that the market share of the new energy car should take 25% by 2025. Besides, the charging infrastructure is another focus amongst different countries. With the high accessible charging station and the development of fast charger technology, the advantages of ICE cars are gradually disappearing.

According to the previous market performance, the market has shown great enthusiasm for the electric vehicle stock. In October 2019, since the Tesla Shanghai Gigafactory has fully started assemblies, the stock price popped 30.7% in October and almost doubled by the end of 2019. With the great sales in 2020, the stock price skyrocketed from $350.5 (before 1 to 5 split) to $607.8 (November 2020), which is an 8.67 times increase. On Nov. 16, 2020, S&P Global announced that Tesla will join the S&P 500 effective before trading on Monday, Dec.21 as the 6th largest company in the U.S. Similarly, the BYD company, which is invested by Berkshire Hathaway, has achieved great success on their electric vehicle products. In Sept 2008, Buffett bet $230 million on BYD and own 25% of the company. Up to the end of Nov 2020, this investment has created around 30 times floating return. In the meanwhile, there are serval days that another Chinese, NIO, had the largest trading volume amongst all the other stock in the U.S. market. At the same time, NIO’s market value exceeded the market value of Audi and chasing for BMW. Many other EV companies showed extraordinary performance in the stock market. Many investors worry that these company’s sales and margin rates cannot support the exorbitant stock price and may become a dangerous investing bubble. However, three company has caught the attention of a great number of U.S investor.

Read full story| Date | Release | Actual | Forecast | Prior |

|---|---|---|---|---|

| Monday | Starting Week of Sept 17 | |||

| Tuesday | ||||

| Wednesday | ||||

| Thursday | ||||

| Friday | ||||